PART I: A NEED FOR DIFFERENTIATION IN VENTURE CAPITAL

If your only impression of Venture Capital (VC) came from what you read or saw in the news, you’d think that VC is a guaranteed way to make money. With “Unicorn” becoming a household term, celebrities like Kobe Bryant and others making millions on their early-stage investments, and VC Assets Under Management (AUM) now above $359 billion it’s not surprising that many people think of VC as an easy way to make money.

However, beneath the tantalizing headlines lies the reality that VC is a structurally challenged and increasingly competitive asset class, across a number of dimensions:

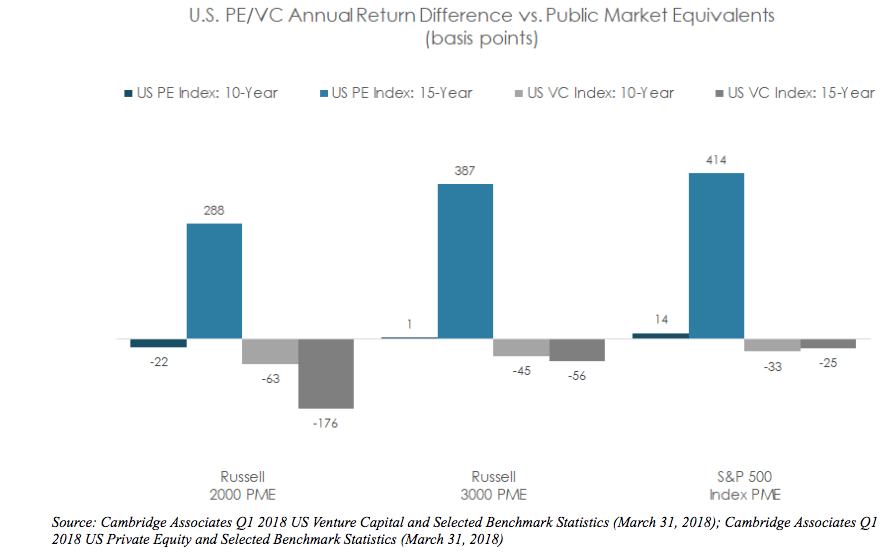

- Performance: VC has underperformed competing asset classes – particularly private equity – as well as its public market equivalents (PMEs), which are measures that normalize VC returns against the opportunity cost of instead investing into a stock index, such as the S&P 500.

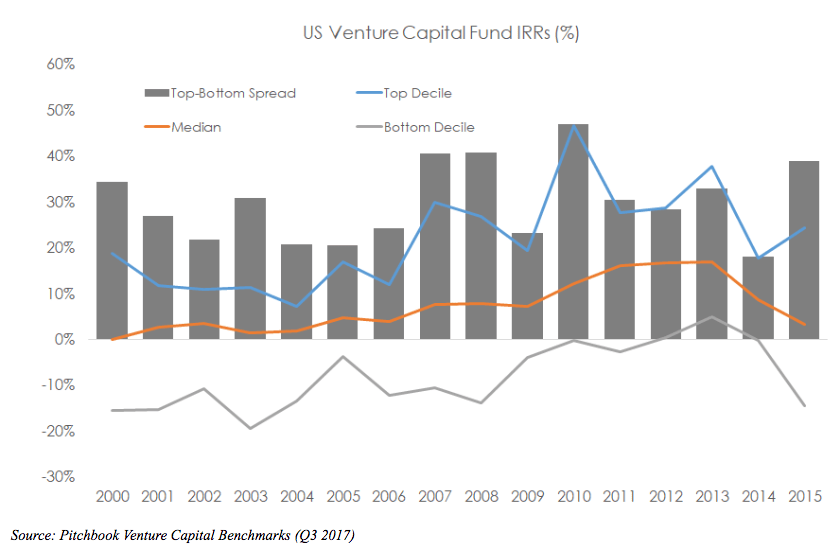

- The Midas Touch: Within VC, top firms continue to produce great funds and attract commensurate media attention. But the significant dispersion between these funds and the rest reflects that in VC, the rich get richer as they capitalize on the virtuous cycles of VC-entrepreneur selection as a result of power law dynamics or persistence of VC investing. The others tend to produce less-than-stellar returns.

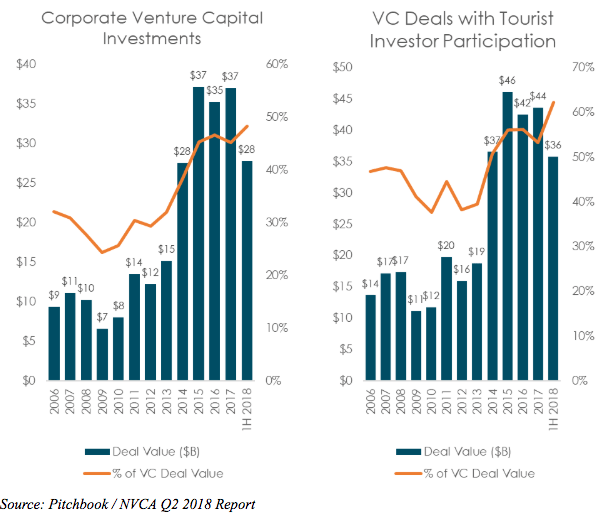

- The Rise Of Non-traditional VC Investors: VC competition has increased over the last few years in part because of a new type of investor entering the fray. The first half of 2018 witnessed record VC investment participation from corporate venture capital and VC “tourist investors” (hedge funds and mutual funds).

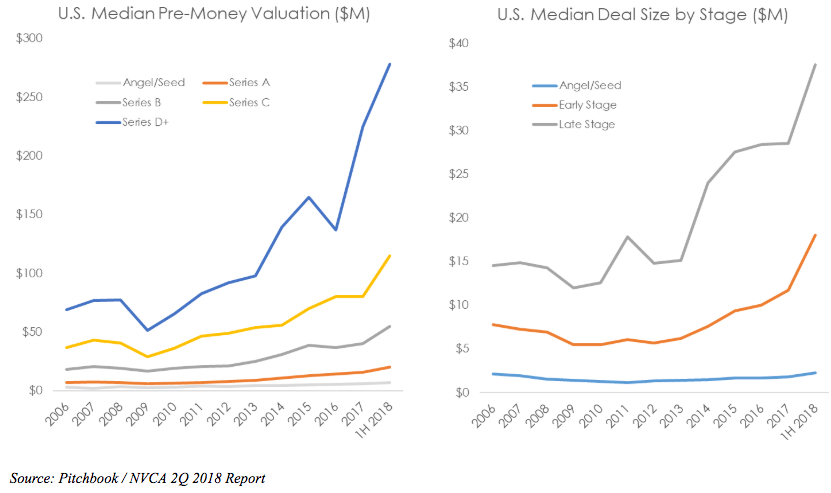

However, the allure of the ‘unicorn’ has led to an enormous amount of funds raised. The result is a massive imbalance between yet-to-be-deployed capital (i.e. “dry powder”) and investment opportunities — an imbalance that is now being manifested in the skyrocketing of valuations and funding rounds, which are at all-time highs across investment stages.

All of the above mentioned factors have made generating above-market returns more challenging. As firms strategically evaluate how to become or maintain elite investor status, the question naturally arises: how can I differentiate myself in ways that actually matter?

In recent years, now prolific firms have emerged as leaders because they answered that question with innovations on the traditional venture model; innovations grounded in the idea of the VC Platform.

PART II: THE AGE OF THE VC PLATFORM

Over the last 15 years Union Square Ventures (est. 2003), First Round Capital (2004) and Andreessen Horowitz (2009) – have differentiated themselves by providing more systematic, tangible value-add through (i) network-harnessing platforms, and (ii) significant portfolio support staff, which both theoretically add value post-close and make their VC firms more attractive to founders.

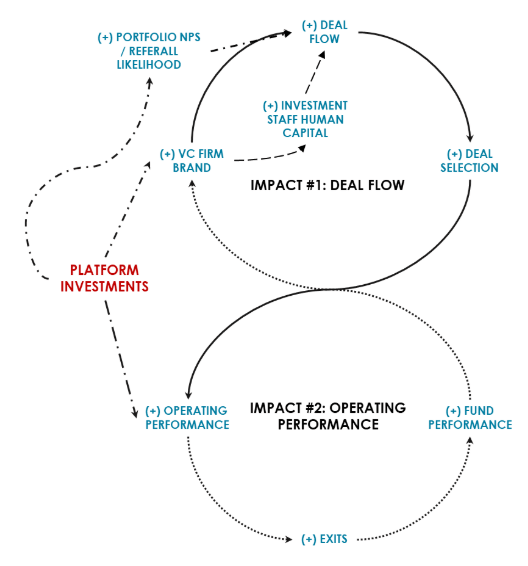

So how does this “platform model” actually work? The logic of the VC platform model in the context of the overall firm functions as follows: 1) The firm makes investments in post-investment resources or support staff (in red below); 2) these investments then lead to a 2-sided positive feedback loop, in which these resources may lead companies to perform better (IMPACT 2) and also generate better deal flow as a result of the firm’s enhanced brand reputation for supporting founders (IMPACT 1). These feedback loops directly and indirectly improve fund performance, and so the positive feedback loop goes on.

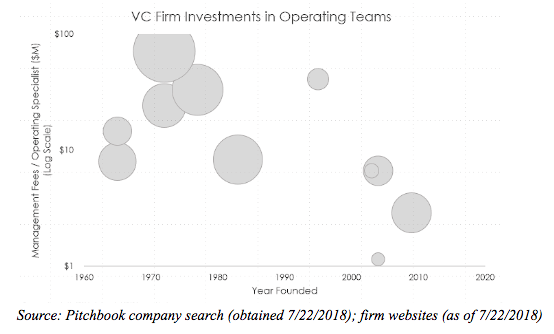

The trend of the VC platform is a visible one; top performing firms that have been established more recently have invested more of their management fees into operating specialists.

Implications for CPG Investing

The rise of the VC platform has mostly taken shape in the world of software investing, where VC is generally more mature. However, the implications for Consumer and Retail VC are significant. Here at CircleUp, these learnings have helped shape our understanding of how to best improve outcomes for our LPs and serve the founders we aim to help. In our next post we will discuss our approach to building a platform to help our companies across all of our products.