At CircleUp, I’ve spoken to thousands of entrepreneurs and founders who are navigating the stressful process of raising capital for their businesses. Many of the early-stage consumer companies that we’re on the phone with everyday are under intense pressure to review multiple term sheets so they can access capital quickly and efficiently for their businesses, often times during periods of immense growth.

It’s become obvious that more and more lenders are hiding costly fees behind an eye-catchingly low “Annual Interest Rate.” After a number of conversations with entrepreneurs who were surprised by hidden fees, we thought it would be helpful to put together a quick resource that puts you in the driver’s seat when evaluating the best working capital financing options for your business.

Look at Annual Percentage Rate Not Annual Interest Rate

APR is what truly matters when evaluating options, not Annual Interest Rate. We see many companies that have term sheets boasting low annual interest rates anywhere from 4 – 8%. However, it’s important to look past that rate and consider how additional fees can make your loan more expensive than it first appears.

Imagine a scenario in which you’re considering a new credit card. The monthly interest rate that you’ll be charged on an outstanding balance is very important, but you might balk at a high annual fee. If Amex tried to charge you an additional origination fee or due diligence fee just for considering your application, you would probably be pretty upset and go with other options. Try and apply this same mentality to any working capital loan.

The key here is to determine the true APR, which can quickly be calculated as:

APR = (Annual Interest + Fees) / Average Capital Outstanding

You can see that while your annual interest rate may be low, this number alone does not determine your APR. Most lenders with low interest rates have other fees built into their term sheets that need to be considered because they can dramatically increase the cost of capital. Compared to a credit card company that is required to quote rates in terms of APR, many financing companies will only quote their annual, monthly, or weekly interest rates, choosing not to broadcast their additional fees up front.

Watch Out For Hidden Fees

Take a close look at any term sheet and you’ll notice there are often a wide variety of fees stacked on top of the initial annual interest rate. At CircleUp, we’ve also noticed that terminology varies by company, so here’s a list of some things to scan for when reviewing any offer:

- Underwriting or Due Diligence Fee

- Management or Monitoring Fee

- Origination Fee

- Processing or Administrative Fee

- Legal & Servicing Fees

- Facility or Collateral Fee

- Wire Fee

- Field Exam or Inventory Review Fee

- Discount Fee

- Early Termination Fee

- Late Payment Fee

- Prepayment Fee

Many of these fees will increase your APR before any capital even hits your account while some will surface over the course of your lending relationship, resulting in a (potentially unexpected) increase in your APR at a later point in time. Either way, make sure to read your term sheet closely and consider all the fees associated with your loan, not just the quoted interest rate. It’s important to always discuss the fees with your lender prior to engaging and ask them to quote you an all-in APR. It’s probably a red flag if they’re unwilling to do that.

Ask A Lot of Questions

We know there’s a ton of information on lending products out there and it’s often easy to get lost down a rabbit hole when researching the best product for you. We hate to see our potential borrowers get tripped up by extra fees that end up costing more over the life of their loan.

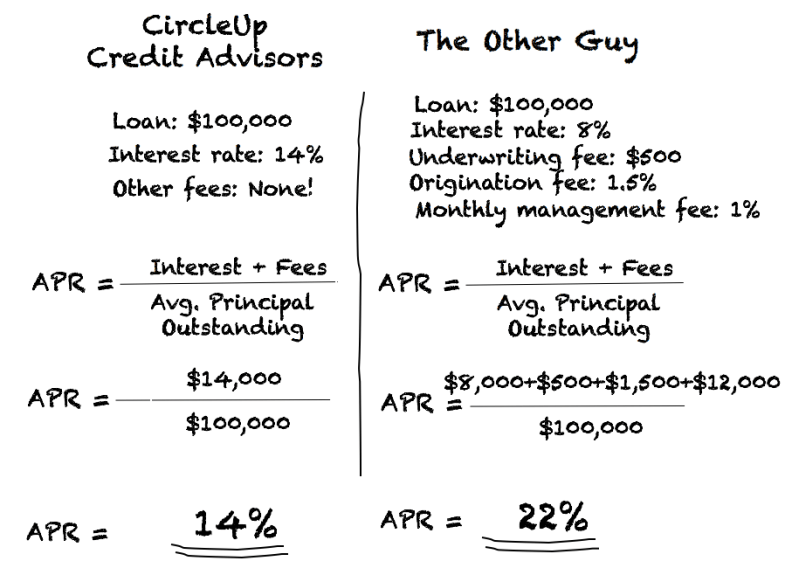

As a real-life example of this, a company we spoke to recently was looking for $100K loan and was quoted an annual interest rate of 8% by another lender. We offered this company an all-in APR of 14%. At first glance the company was surprised by the difference, but looking a step further, it turns out the other lender was going to charge the company an additional $500 underwriting fee and a 1.5% origination fee on top of their $100K loan. They would also have to pay a 1% monthly management fee. 1.5% and $500 don’t exactly seem like a lot, but when you add up the numbers to determine the full APR using the formula from above, you’re left with a pretty surprising result –– see below:

Looking at the two APRs side by side helps put the other guy’s offering in a new light.

So there you have it. A quick and easy way to determine and compare APRs. (As a plug, CircleUp Credit Advisors always communicates and explains all-in APR rates with all prospective borrowers)

If you ever have any questions or want to discuss your financing options further, feel free to give our team a shout! We’re always here at credit-bd@circleup.com