/Hero%20Backgrounds/Gradient-Sun-med.jpg?width=300&name=Gradient-Sun-med.jpg)

By:

By:

This guest editorial comes to us from Christopher Orr, Director of Institutional Products at PENSCO Trust. PENSCO is a leading alternative asset custodian, with more than two decades of expertise in holding private equity, real estate, notes, and other non-exchange traded assets.

The world of private equity isn’t quite as private anymore.

Equity crowdfunding, a form of private equity investing that allows accredited investors to purchase equity in a business or a fund, is growing in popularity. According to Crowdnetic, more than $480 million has been committed through equity crowdfunding since the JOBS Act went into effect, and crowdfunding sites now allow investments in everything from real estate to movies to personal care products.

The growth of equity crowdfunding and the media attention it has attracted means that more Americans are becoming aware of private equity and how it can fit into their portfolios. But when many people consider investing in private equity — whether it’s through an equity crowdfunding site or not — their first instinct is to invest with taxable dollars. That’s because many investors do not realize they can also invest in private equity using tax-advantaged dollars in their IRA.

Given that it’s tax season and many investors are considering their tax strategies for 2015, it’s a good time to understand why you might want to invest in private equity using retirement dollars.

Private equity investments, while risky, can deliver higher returns than public equity markets. According to data from the Private Equity Growth Capital Council, private equity investments delivered average returns of 14% in the 10 years ending in 2013, compared with 7.4% for the S&P 500. If you invest in private equity using retirement funds, you’ll gain tax advantages. Holdings in a traditional IRA can compound year after year on a tax-deferred basis and can grow that way until required minimum distributions must start when the account holder is 70½. If you made this investment using a Roth IRA, the account growth would accumulate tax free.

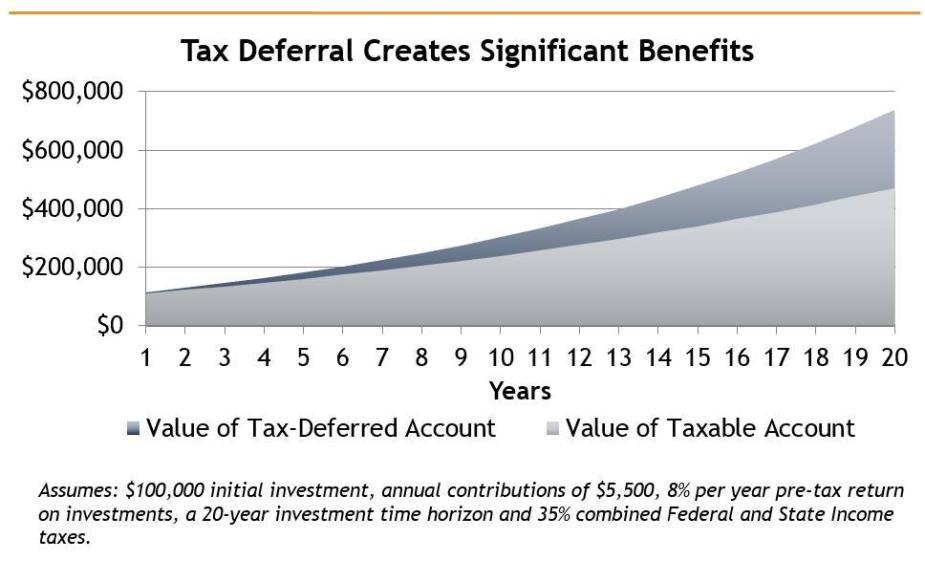

This can create a powerful advantage over time. This chart captures the growth trajectory of $100,000 invested in a taxable account vs. a tax deferred account over 20 years.

The tax deferred account reaps the benefits of greater compounded interest and returns because they are not being eroded by taxes. If you contributed $5,500 a year and made an 8% return, you would have nearly twice as much money at the end of 20 years in a tax deferred account than you would have in a taxable account.

Given that retirement funds tend to have inherently longer time horizons, they can be a good match for private equity investments, which also can require long holding periods.

Of course, all investments come with their risks, and private equity is no different. It’s crucial to do your due diligence on any investment opportunity or work with a financial professional whom you trust before pursuing these opportunities.

This article does not provide investment, tax, or legal advice nor does it evaluate, recommend or endorse any advisory firm or investment vehicle. Investments are not FDIC insured and are subject to risk, including the loss of principal.

ABOUT THE AUTHOR:

Christopher Orr is a Director, Institutional Products, at PENSCO, where he has spent the past five years helping clients meet their retirement savings goals by using self-directed IRAs. Christopher uses his broad financial services expertise to help high net worth clients, advisors and asset sponsors accomplish their private equity investing goals using self-directed IRAs.