/Hero%20Backgrounds/Gradient-Sun-med.jpg?width=300&name=Gradient-Sun-med.jpg)

In the past quarter I’ve seen a marked increase in interest in CircleUp’s asset class, early stage consumer, from institutional investors.

Having built a platform to identify, evaluate and fund early stage non-technology opportunities at an unprecedented scale, we pride ourselves in having greater access to data on the early stage consumer market than anyone in the world. In the past two years alone we’ve reviewed more than 7,000 funding applications; and since mid-2012 more than 80 companies have successfully raised through CircleUp. That’s more successful consumer and retail fundings than any other source of capital in the country during that period.

While individual investors often look to specific companies for investment opportunities on CircleUp, institutional investors want scale. Strong performance. Diversification. And a compelling, data-driven thesis on why they should deploy capital across CircleUp versus other alternative asset classes. Like our individual investors, they are sophisticated, but maintain a broader lens when looking at our platform. Since we have had many of these conversations recently, I wanted to share some of the thinking we see from these large investment managers.

Here are the two questions that I hear most often.

- What are the trends driving early stage consumer?

- How does your asset class fit in a broader portfolio? (Read: Why should I have exposure here?)

Trends: Shifting Millennial Tastes

We see strong macroeconomic tailwinds behind early stage consumer brands. There is a large shift in consumer preferences from large brands to smaller brands.

The data on the growth of small brands is eye opening. In a report released by Jeffries, “Food: The Curse of the Large Brand.”, Jeffries found that large brands lost share to small brands in 42 of the top 54 food categories in the last five years.

“The majority of the branded packaged food companies in our coverage show declining market share in scanner data. The likely culprit is a growing disinterest in mainstream processed food brands esp. among Millennials. Large brands across most relevant packaged food categories are declining in scanner data while small, nichey brands grow.” – Thilo Wrede, Jeffries

The shift in consumer preferences, and subsequent rise of small, niche brands, has been severe—and left many ‘Big Food’ companies scrambling to adapt. Many are becoming more acquisitive too:

- Krave Pure Foods acquired by Hershey (HSY) at reported multiple of 9x sales;

- Plum Organics acquired by Campbells;

- Big Heart Pet Brands acquired by J.M. Smucker Co. (SJM); and

- Applegate Farms LLC is reported to be in acquisition talks with Hormel Foods Corp, in a deal that’s reported to be worth up to $1B.

The Deal recently reported from an industry conference where Mondelez (MDLZ), Hains (HAIN), Smuckers (HSY), Campbells (CPB), Kelloggs (K) and General Mills (GIS) all went on the record as saying they are actively looking for takeover targets.

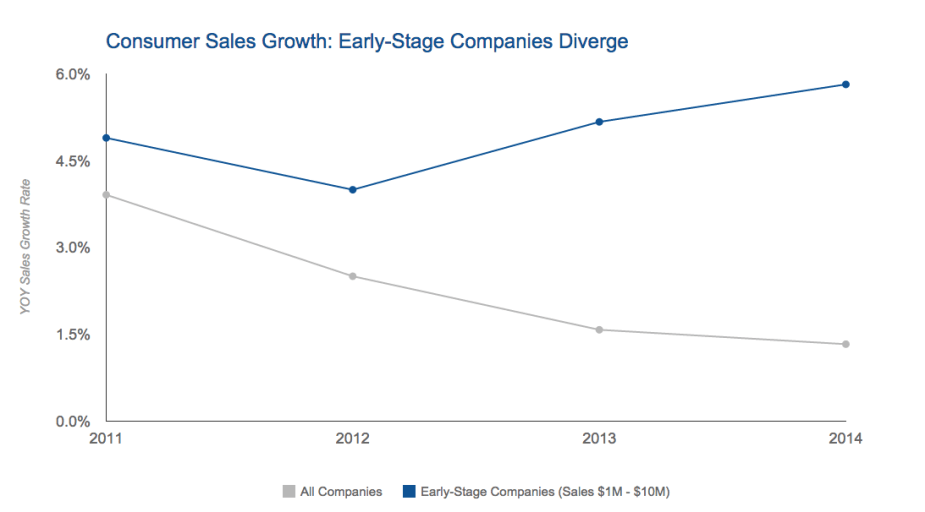

We dug deeper. This trend is broader than just food- it is across all major consumer sectors. Partnering with The Nielsen Company, which gathers retail level sales data, we analyzed the sales growth of small brands versus their parent categories. Between 2010 – 2014, early-stage companies (revenues $1M – $10M) markedly outperformed their peers, achieving an compound annual growth rate (CAGR) equal to 2x the broader Consumer category.

Early Stage Consumer in a Broader Portfolio

In addition to questions about sector level drivers, we also receive a number of questions around how the asset class fits in a broader portfolio. In particular, many institutional investors want to know how the asset will perform relative to others if the economy goes south, or there is an external shock such as high inflation.

We think about this from a few different directions:

Public Market Data

Because time series data in the private market can be difficult to obtain, we looked at public market comparables – specifically micro-cap (Revenues < $200mm and Market Cap > $50M) indices. Food, Beverage and Household & Personal Products sectors, the focus of our marketplace, outperformed similar-sized micro-cap public companies in Luxury & Leisure, Software & Tech and Healthcare sectors over 10 years, 20 years—and have lower betas (a measure of volatility).

Perhaps more importantly for some investors, the micro-cap food, beverage, household & personal products indice showed more resilience than other sectors studied during the downturns in 2001-2 and 2008-9. We believe the reason is that when the economy slows, or moves to a recession, small consumer companies can still grow rapidly by growing more distribution, whereas large brands have already saturated the market, and other micro-cap companies tend to be more vulnerable to pull backs (luxury goods) or are inherently higher beta (technology). While an imperfect correlation with private markets, we believe this data is representative of the strength of early stage consumer and the trends Jeffries notes in the report above.

https://cloud.highcharts.com/embed/eramos

Methodology: For each Micro-cap Sector outlined above, we defined 4 Time Cohorts 1995-99, 2000-2004, 2005-2009, 2009-2014. We defined ‘Micro-cap’ as public companies with Revenues < $200mm and Market Cap > $50.

GICS Industry Classifications

(1) Beverage, Food Products, Household & Personal Products

(2) Leisure Products, Textiles Apparel & Luxury, Specialty Retail

(3) Software & Services, Technology Hardware & Equipment

(4) Healthcare

(5) Financials

Against the Consumer Price Index, US Micro-cap Consumer companies also showed a substantially lower beta than later-stage companies.

Private Market Data

Cambridge Associates

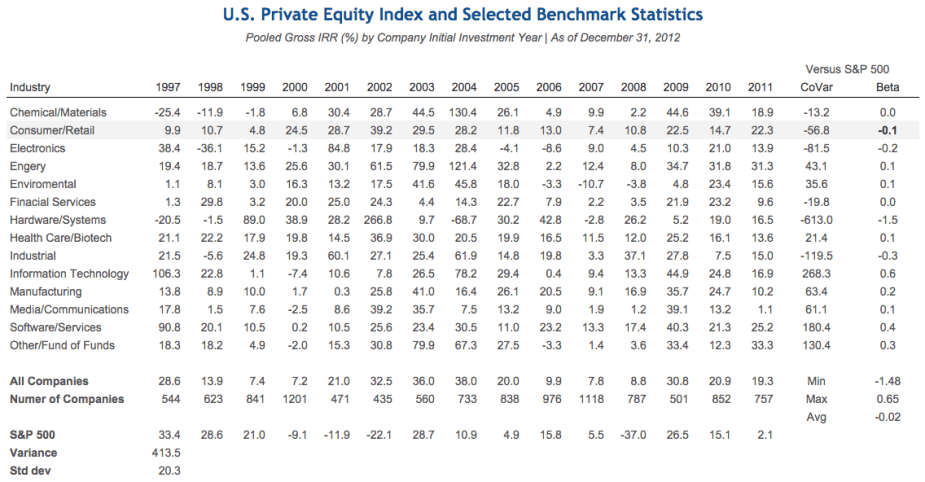

Consumer shows lower volatility in the private markets as well. We looked at this from two perspectives. First, using Cambridge Associates data, we reviewed pooled gross IRR since inception for companies receiving funds from private equity firms from 1997-2011. Cambridge tracked 13 different industries that received PE during this time. Consumer/Retail showed lower volatility than more than half of the industries covered in the study.

IT, Hardware/Systems and Software/Services had the largest three betas in the data set (measured by greatest distance from 0). The substantial beta difference versus Consumer/Retail is interesting because this sectors accounts for the lion’s share of early stage funding in the US today. In this landscape, we believe CircleUp offers a unique low beta, early-stage product that differs from traditional venture capital. (The disappointing performance of venture capital over the last 20 years is a topic for another post. Or a novel.)

Nielsen

With our partners at Nielsen, we looked at data the performance of smaller brands (sub $10M in revenue) vs. all others in a variety of consumer categories. While only a limited data set, this view gives us the best look at how the asset class may perform during a period of higher inflation (the conclusion is also supported by the longer series public market data cited above as well).

Source: Nielsen | CircleUp Research

In addition to the data, why do we believe consumer companies adapt to inflation better than peers? Consumer products are high velocity and low cost, allowing them to quickly adjust prices to maintain margins during an inflationary period. Compared to other industries, a rise in input prices is more easily passed on to end consumers. This conclusion is also supported by the longer public market data set cited above, as small consumer sales were more resilient during downturns in the market.

Summary

Reviewing the data, we believe there is a strong case to be made for including early stage consumer in a well diversified portfolio. A reasonable question is: “if the returns are strong, why hasn’t this been done before?”

Paradoxically, the asset class may be a great opportunity for investors, but not one for professional investment managers. Unlike with technology companies, early stage consumer companies are spread all across the country. Prior to CircleUp, it would take considerable expense to source, evaluate and invest in a broad portfolio of such companies. The VC/PE fund approach has been the dominant model for larger investors to access private investments—however, the fund economics don’t work for a small fund to invest in $1-3M opportunities dispersed across the country.

An online marketplace—free from geographic constraints—can solve these issues, and provide investors, both large and small, with deal flow, data and transparency to intelligently invest in an asset class previously unobtainable.

The private capital markets are opening. Becoming more efficient, and transparent, which stands to benefit investors and entrepreneurs everywhere.